Recession risks, rates and inflation, valuations, geopolitics, the US election and Swiftonomics

Key points

– Rate hikes have worked in helping slow inflation and rate cuts are likely this year. Expect a bumpy ride though.

– The risk of recession remains high at around 40% in the US and Australia.

– Geopolitical risk including around the US election remains high but it’s often easy to get gloomy regarding geopolitics.

– Share valuations are a bit stretched pointing to the risk of more volatile and constrained returns, but shares should ultimately be okay as interest rates come down.

Introduction

Last year shares climbed a “wall of worry” as inflation fell leading to prospects for lower interest rates ahead. But can it continue? After participating in a webinar on the investment outlook this note takes a look at the main questions investors have in a simple Q&A format.

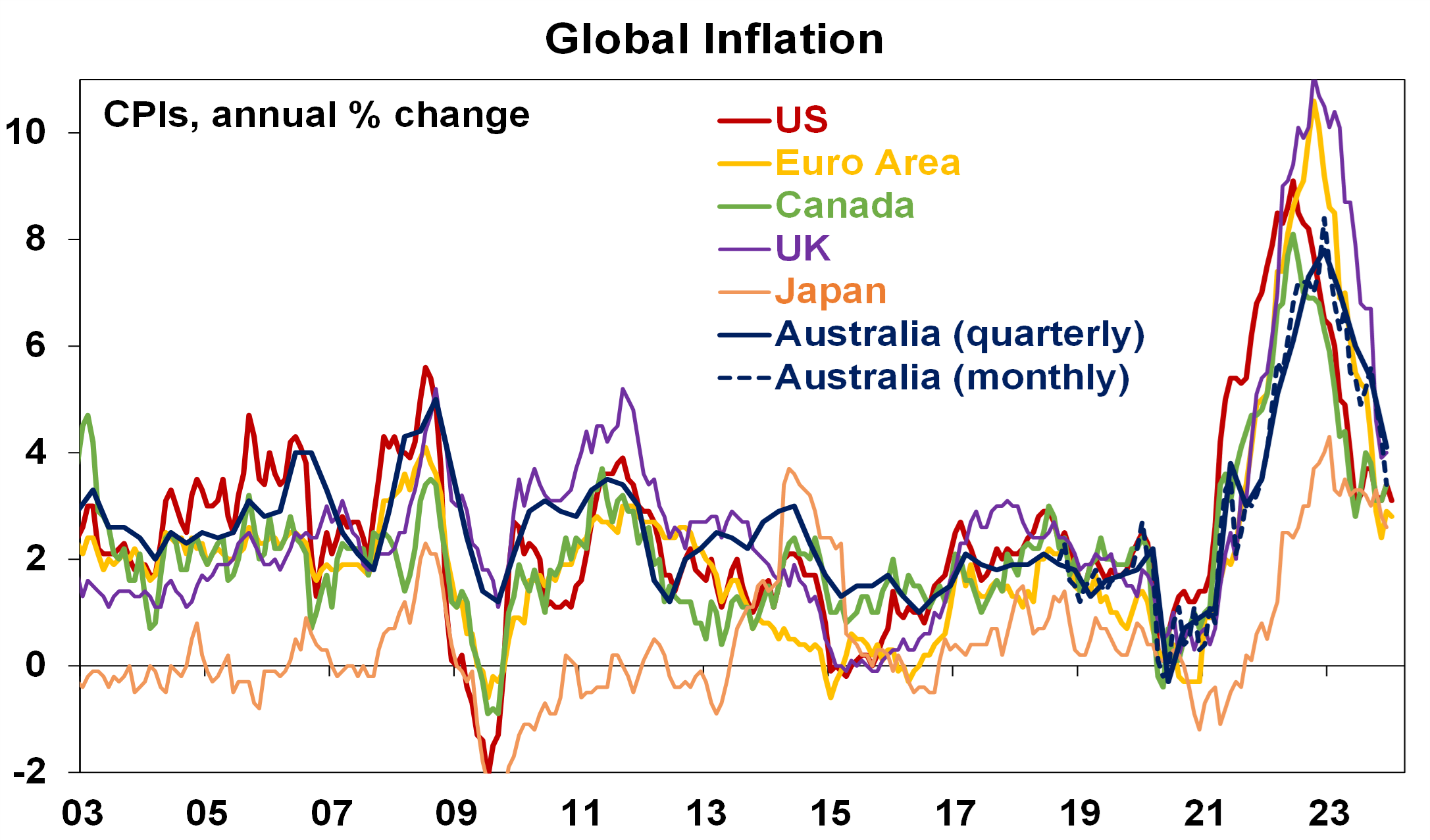

Are high interest rates working to cut inflation?

The evidence of this is overwhelming. Inflation has fallen from highs around 8 to 11% in major developed countries, including Australia, to now around 3-4%. This reflects a combination of the improved supply of goods and services as well as cooler demand (evident in cooling economic growth and slower labour markets) and higher interest rates have been a key driver. There has further to go and it will be bumpy as we saw with the January US CPI, but central banks are likely to start cutting interest rates in the June quarter with the Fed and ECB expected to cut 5 times this year (by 0.25% each time) and the RBA 3 times.

Source: Bloomberg, AMP

But aren’t high rates unfair? Isn’t there a better way?

Relying on higher interest rates is not the only or fairest way to slow inflation because it particularly hits 25 to 45 year olds with big mortgages. Ideally the medicine should also involve a mix of tighter fiscal policy (tax hikes and public spending cuts) and structural policies to boost productivity and hence the supply of goods and services. But it’s clear governments don’t want to tighten fiscal policy because it’s not politically popular (if anything they want to provide “cost of living relief”) and supply side policies take time to work and aren’t popular these days either. So after the experience of high inflation in the 1970s, it was concluded that central banks are best placed to control inflation and they really only have one main tool – i.e. higher interest rates.

What is the risk of recession?

Global and Australian growth has held up far better than expected a year ago helped by a combination of savings buffers built up through the pandemic, reopening boosts, resilient labour markets and in Australia far stronger than expected population growth (which has masked a per capita recession). Consequently, while global and Australian growth has slowed it has remained positive. Our base case is for a further softening in growth but for it to remain positive ahead of lower interest rates providing a boost from later this year.

However, the risk of recession remains high after what has been the biggest rate hiking cycle since the 1980s and this being reflected in inverted yield curves (short term rates above long term bond yields), falling leading economic indicators and tighter bank lending standards all of which warn of the high risk of recession particularly as some of last year’s supports like saving buffers, reopening demand and very strong population growth in Australia start to fade. So we put the risk of recession at 40% in Australia and the US. Europe is already close to recession having been stagnant GDP over the last year. China is also a risk – see below. Fortunately, if a recession does occur it’s likely to be mild as most countries have not seen a boom in consumer spending, business investment or housing investment that needs to be unwound.

Will Taylor Swift shake off Aussie consumer gloom?

For the next two and half weeks it will certainly help for the roughly 630,000 concert goers and the retailers, hotels, and food outlets that will get some extra spending. If each attendee spends a total of $900 on average (which sounds generous) it will mean spending of $570m which is a lot of money. But it won’t take us out of the woods because Taylor is an import and so maybe only $400m of that will stay in the country. And $400m is just 0.02% of our economy. And as Governor Bullock implied it will likely come at the expense of other things. So maybe a two-week blip and then back to where we were. In other words, if you are all excited about Swiftonomics you need to calm down. That said I am excited about finally getting a ticket…even if it is one of the partially obscured seats.

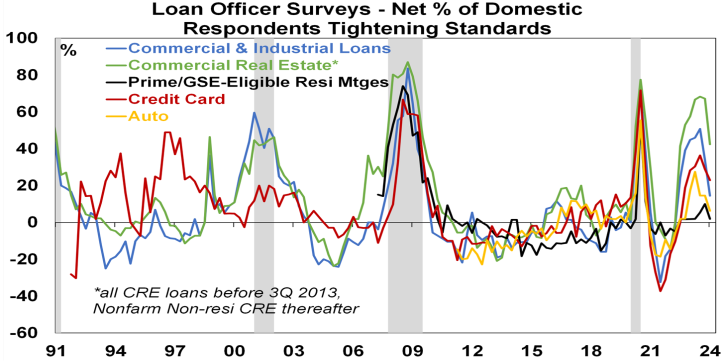

What happened to US bank problems?

Quick action by US and Swiss authorities settled the banking problems seen last year and the tightening in lending standards associated with it has eased. In the US, the Fed’s December quarter bank lending survey showed less tightening in lending standards and loan demand becoming less negative, which suggests an easing in regional banking problems. But with monetary policy still tight and ongoing falls in commercial property values the problems could return – as seen with New York Community Bank and Japan’s Aozora Bank recently. So, it’s worth watching.

Source: Bloomberg, AMP

What about China and Evergrande’s liquidation?

China faces three big challenges: a falling population; trying to get consumer spending to take over as a key growth driver from capital investment and the property sector; and political tensions with the West. Taken together they imply a slowdown in China’s long term growth rate.

In the near term the property slump continues. But a Hong Kong court ordering the liquidation of property developer Evergrande is not going to trigger a Lehman moment that will turn China’s property downturn into a global crisis. First, it’s not a big surprise. Second, it’s doubtful that PRC courts will allow liquidators to sell Evergrande assets in China in a fire sale given the Chinese Government’s focus on protecting home buyers and completing more homes. Finally, the Chinese Government will continue offset any impact from the property downturn and Evergrande’s woes on the economy with property and economy wide stimulus measures.

Overall, we see Chinese growth as being constrained with downside risks – but it’s likely to be around 4.7% this year with the Government providing just enough stimulus. It’s hard to have a strong view on Chinese shares but their bear market may be nearing an end. After having nearly halved since October 2021 they are now undervalued (with a forward PE below 10x), oversold & underloved and due at least a further bounce.

How big a threat are geopolitical risks?

Geopolitical risk is high this year: with half the world’s population seeing elections; the US looking like another divisive Biden v Trump election on the way; tensions with China remaining high; the war in Ukraine continuing; and an ongoing escalation in the Israel/Hamas war to include other countries in the region including Houthi rebels disrupting Red Sea shipping with a risk that further escalation could threaten global oil supplies. Trying to quantify what these mean for the global economy and investment markets is impossible – as we saw last year geopolitical risks turned out to be less threatening. But odds are that they will contribute to a more constrained and volatile ride in investment market this year.

What about the US election?

A Trump victory could lead to considerable global uncertainty given his style of governing and trade policies but this may not be immediately apparent because the US election has a long way to go yet and both Biden and Trump could drop out, US presidential election years historically see average share market returns and after the 2016 Trump victory shares rallied with 2017 being a strong year because of Trump’s pro-business policies (the trade war didn’t start till 2018).

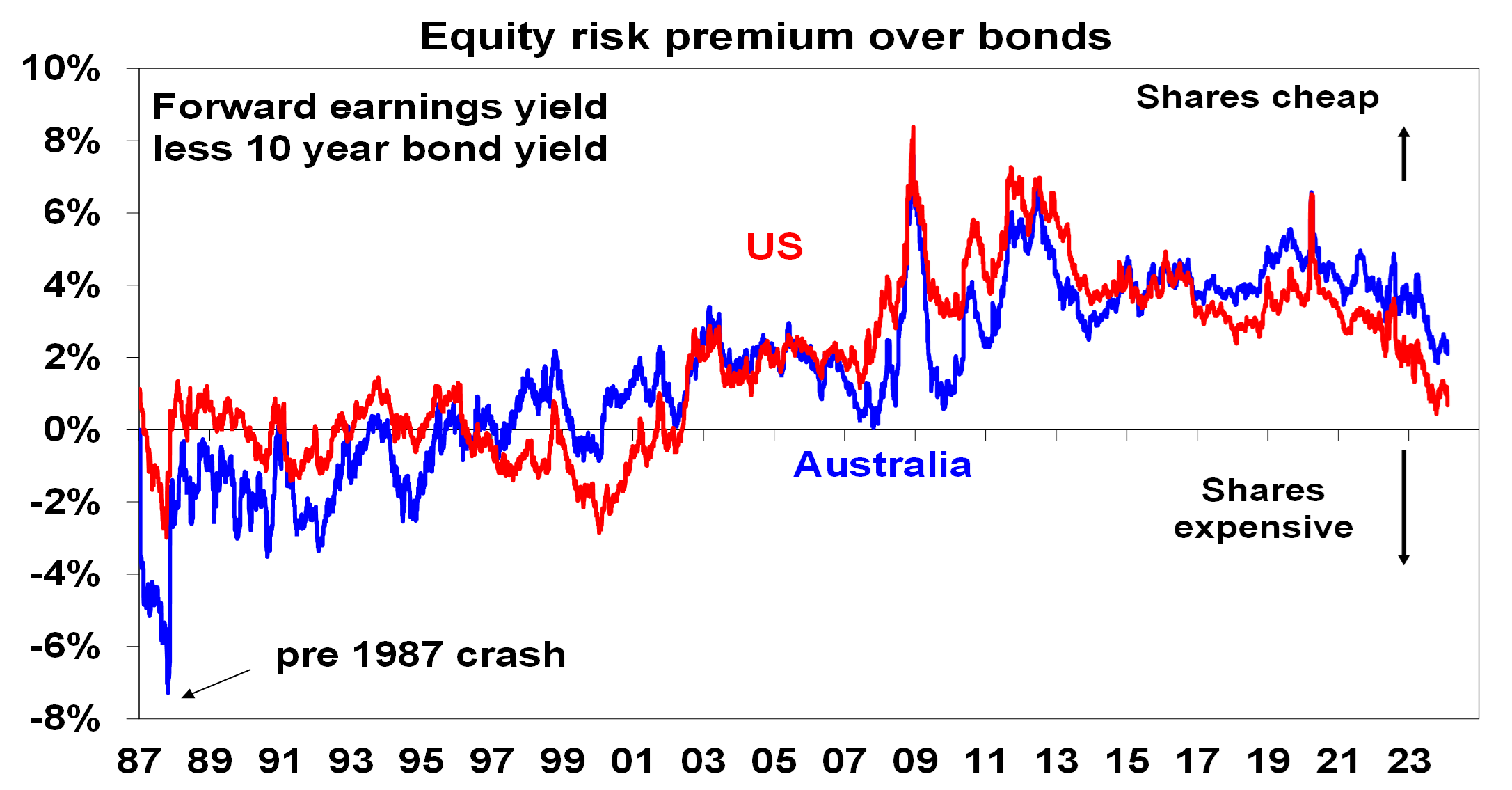

What about share valuations?

Shares are not cheap with above average forward PE’s and a lower risk premium on offer over bonds than seen over the last decade – which leaves shares a bit vulnerable given the high level of economic and geopolitical risks which will likely contribute to volatility. However, the risk premium is a bit higher than it was last October thanks to lower bond yields and shares should be okay providing central banks cut interest rates this year and the profit outlook improves.

Source: Bloomberg, AMP

What will happen to bond yields if interest rates fall?

If as we expect economic growth slows, inflation falls further and central banks cut interest rates then bond yields are likely to fall a bit this year. Of course if there is a recession, central banks are likely to cut interest rates more than we are allowing and bond yields will likely fall a lot pushing up bond values and see bonds be a good portfolio diversifier.

Will high levels of global debt de-rail things?

Global debt is now estimated to be around $US310trn or 340% of global GDP. This clearly poses a threat if bond yields resume rising which will be a big problem in emerging countries with $US debt but will also ramp up pressure for fiscal austerity in rich countries as debt interest payments rise. However, much of the rise in debt since the pandemic has been in the public sector where the risk of major problems is less (as governments can raise taxes), and most advanced country governments borrow in their own currency heading off foreign exchange crises.

How close is America to breaking?

It’s easy to look at the political polarisation, inequality and rising public debt in the US and get depressed. Then again people have long been looking at the US and getting depressed, but it seems to keep on keeping on. It has a very dynamic economy, its productivity growth is impressive, it continues to have world beating tech companies, its growth rate has been surprising on the upside, and it still has very low unemployment.

Why are rich countries running high immigration?

Part of this is a catch up after low immigration in the pandemic but it has been a bit out of control and does run the risk of a political backlash as it accentuates already expensive housing.

When will the $A get back to $US0.80-$US1?

We see upside in the $A to $US0.72 as the Fed cuts rates more than the RBA, commodity prices remain in a long-term upswing and the $US falls on hopefully reducing global uncertainty. However, a move much beyond that looks unlikely given slowing growth in China and geopolitical risks.

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

![]()