Key points

– At its December meeting the RBA left rates on hold but retained a tightening bias with still relatively hawkish commentary.

– Our concern remains that the RBA has tightened more than necessary with a high risk of recession next year. The key risk remains consumer spending where various indicators continue to point down.

– The risk of another rate hike – which if it occurs would most likely be at the next meeting in February after December quarter inflation data – remains high at around 40%

– However, our base case is that the RBA has reached the top and we see it cutting rates in second half 2024.

Introduction

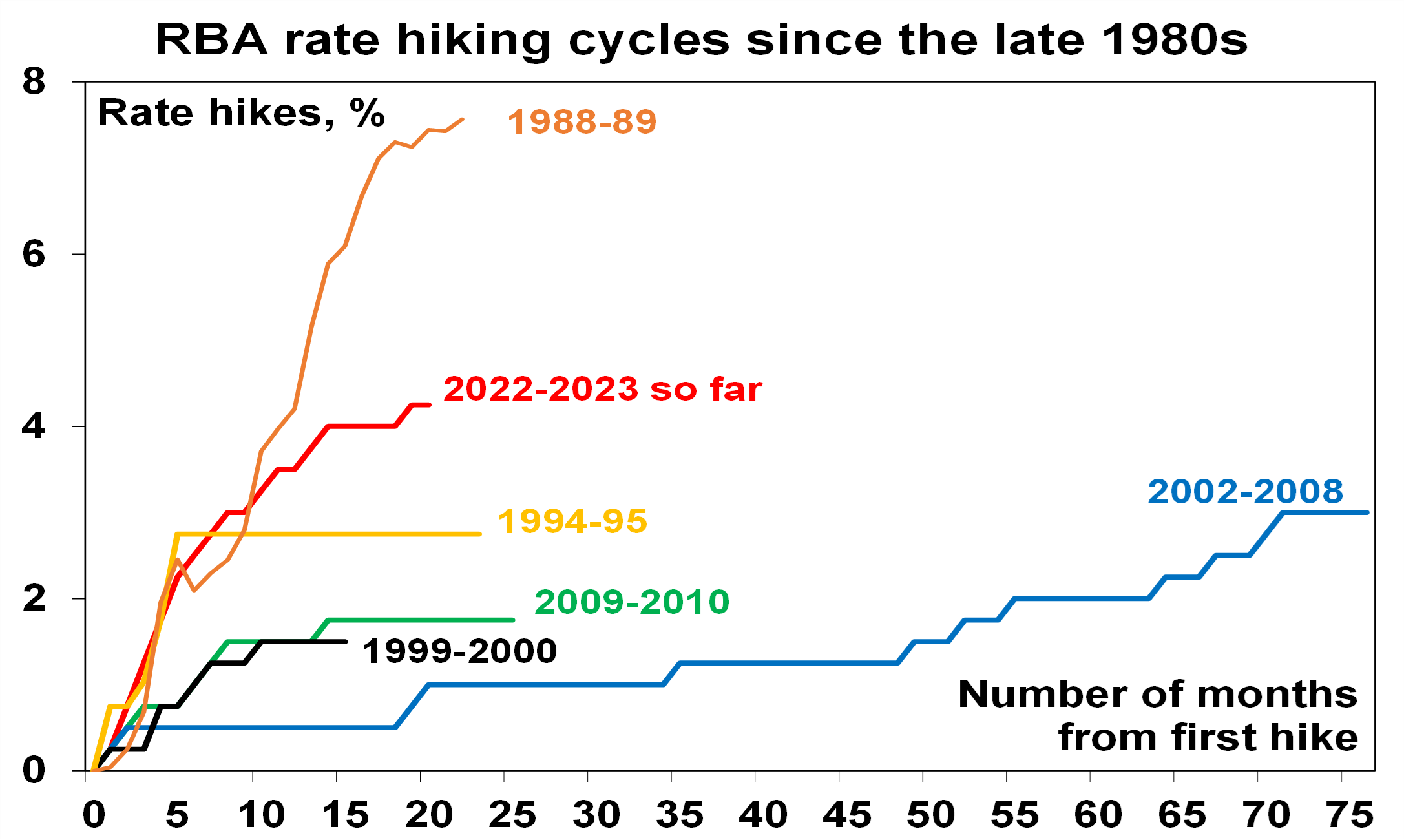

At its December meeting the RBA left the cash rate on hold at 4.35%. This was in line with our own view & that of most economists along with money market expectations. It followed a 13th hike at its November meeting which meant a total of 425 basis points over 19 months since May last year, which has been the biggest interest rate hiking cycle since the late 1980s.

Source: RBA, AMP

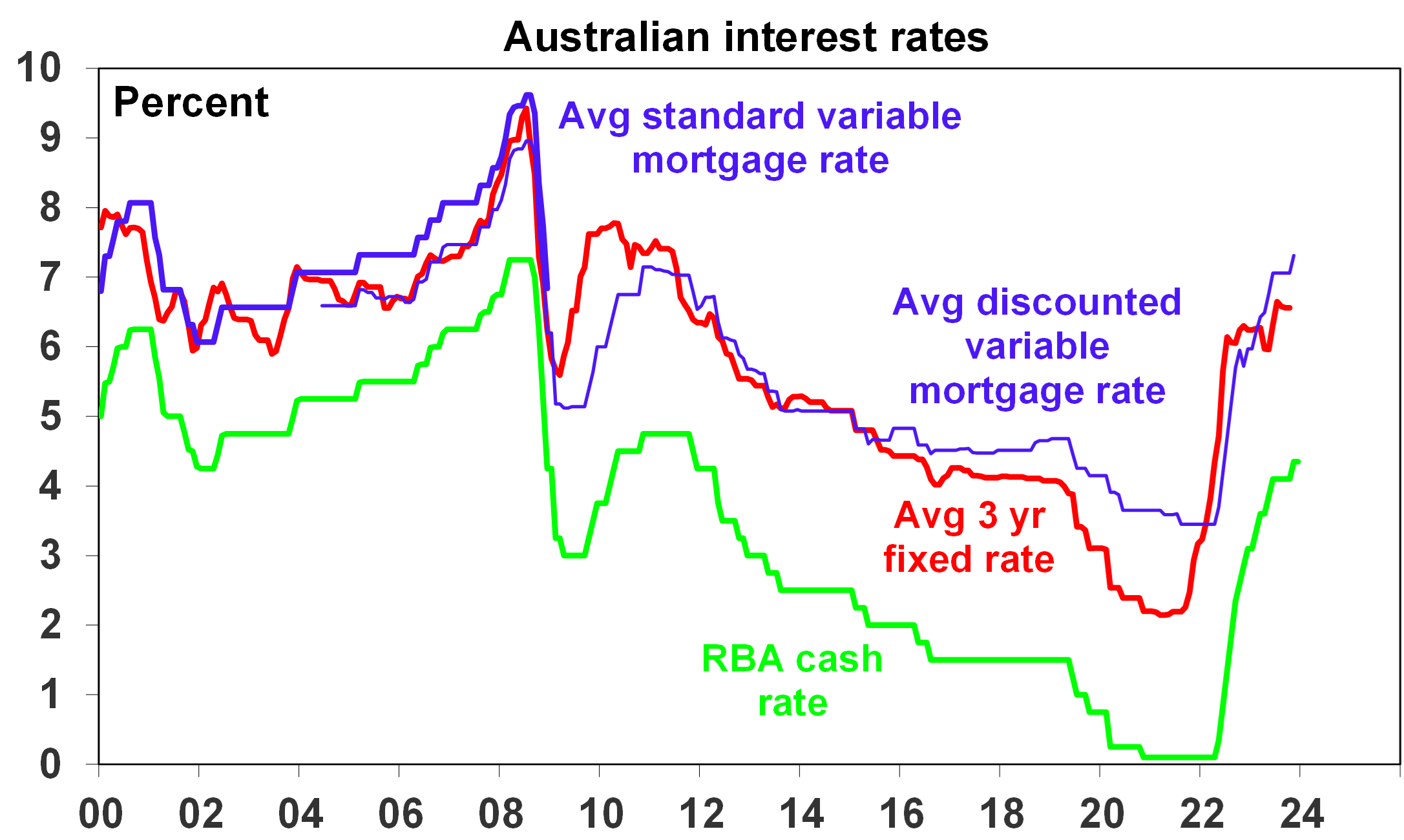

This took the cash rate to levels last seen in 2011 and mortgage rates to levels last seen in 2008.

The RBA retains a tightening bias

The RBA no doubt considered again whether to hike or hold before opting to hold. In this regard it noted that since the last meeting new information has been broadly in line with their expectations, the October CPI suggests inflation continues to moderate and it doesn’t expect much further rise in wages growth. However, it continues to stress the importance of returning inflation to target and keeping inflation expectations down and remains concerned about sticky services inflation with the jobs market easing but still tight. While the RBA retained the softened wording from the November meeting that “whether further tightening of monetary policy is required…will depend upon the data and the evolving assessment of risks” it’s clear that it retains a bias to raise rates again.

There is no meeting in January but by the February meeting the RBA will have December quarter inflation data, two more rounds of retail sales and jobs data and revised RBA forecasts – so all of these will be critical. Given its hawkish bias our view is that the risk of another rate hike remains high at around 40% – and if it occurs it will be at the February meeting.

The case for rates being at the top

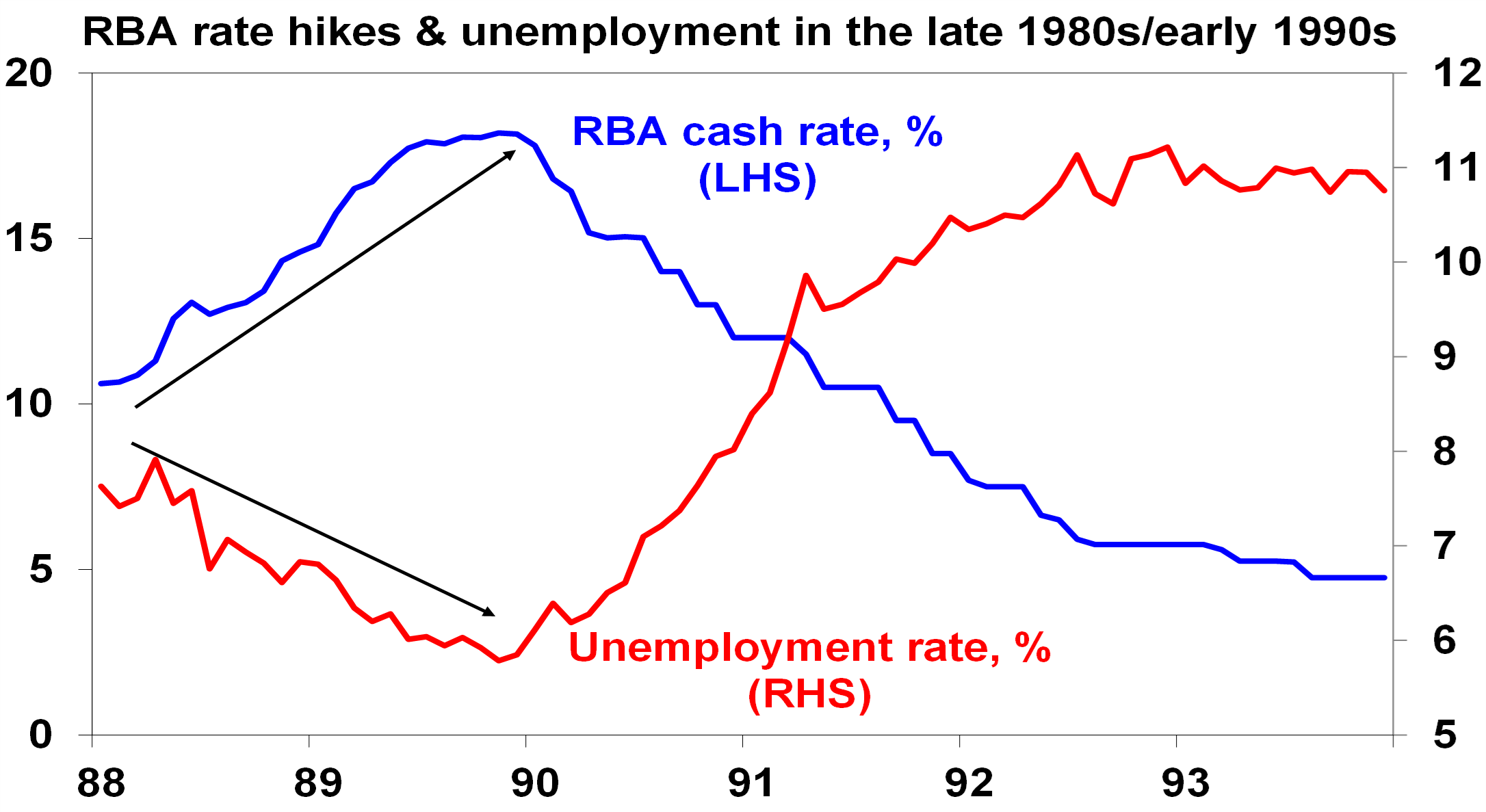

We have been way too optimistic as to how far the RBA would raise the cash rate, but our view remains that the RBA has done more than enough to bring inflation back to target and that we are likely at the peak in rates.First, while the economy has been far more resilient than we expected when rate hikes started 19 months ago its well known in the words of Milton Friedman that “monetary actions affect economic conditions only after a lag that is both long and variable”. This can be up to 18 months or more. This is because it takes a while for the hikes to be passed through to borrowers and for them to adjust their spending and for this to impact companies and jobs. The experience of the late 1980s in Australia where the cash rate was raised from 10.5% to 18% though 1988 and 1989 but unemployment kept falling, only for the economy to fall into recession in 1990 is a classic example of these lags at work. (Rates were higher then, but the level of household debt to income was one third current levels.)

This time around the lag has likely been lengthened by savings buffers built up in the pandemic, the reopening boost, more than normal home borrowers locking in at 2% or so fixed rates and “labour hoarding” boosting employment. However, these protections are likely now wearing off.

The 13 rate hikes since May last year mean that a variable rate borrower with a $600,000 mortgage will have seen around an extra $17,000 a year added to their mortgage payments. Most may have sought a better deal but even if they got a 0.5% discount on their mortgage rate it would now amount to an extra $14,900 in extra mortgage payments. This has already seen housing debt interest payments as a share of household income double from their lows with scheduled total payments rise to a record share of income. It’s hard to see this not having a big impact on household spending. Particularly given the RBA’s analysis based on variable and fixed borrowers that around one in seven households with a mortgage were already cash flow negative in July, which will likely be higher by now.

Secondly, while the data is noisy, we are seeing ongoing evidence that rate hikes are biting with real per person retail sales down 4% on a year ago and the ABS’s Monthly Household Spending Indicator pointing to now falling real consumer spending, a sharp fall in building approvals from their highs, slowing business investment plans, job vacancies well down from their highs, unemployment starting a modest rising trend and now signs that home price gains are slowing again. Combined this is likely to continue to bear down on underlying inflationary pressures. And while a surge in petrol prices was a concern a month ago global oil prices have since turned down again and this is flowing through to lower petrol prices.

Source: ABS, AMP

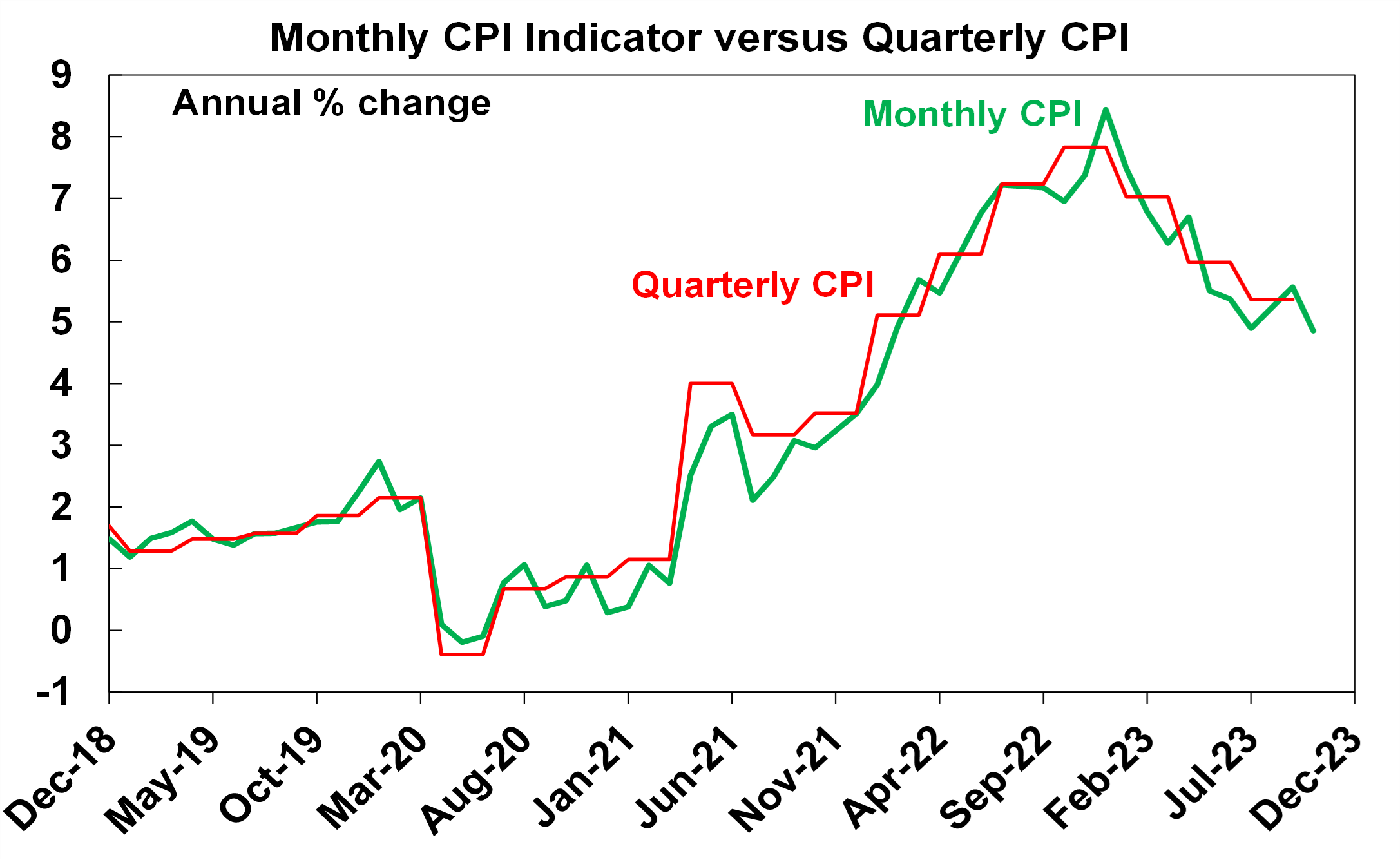

Thirdly, the news on Australia inflation has improved after a setback in August and September and points to an ongoing fall. The Monthly CPI indicator for October came in far less than expected at 4.9%yoy, down from 5.6%, with an implied monthly fall of 0.3% mom. Of course, the monthly CPI can be very volatile, various subsidies impacted in October, key services (like hairdressing, dental and pet services weren’t measured) and underlying measures of inflation fell by less so there is a case to be cautious, but the good news is that the downtrend looks to be resuming.

Source: ABS, AMP

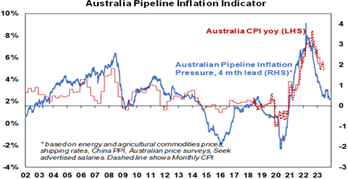

Consistent with this, our Australian Pipeline Inflation Indicator points to a further fall in inflation ahead.

Source: AMP

In fact, monthly inflation could have a three in front of it by December. While some fret that Australian inflation is now well above the circa 3% yoy rates that apply in the US, Canada and Europe it should be recalled that Australian inflation lagged on the way up and peaked three to six months later and it’s doing the same on the way down so there is no reason to be alarmed that its currently higher. In fact, with monthly rises in November and December 2022 of 0.9% mom and 1.5% mom to drop out respectively in the next two months’ CPI releases we are likely to see monthly inflation with a three in front of it by year end. This will bring Australian inflation more into line with US, Canadian and European inflation.

Fourthly, the decline in global inflation points to a broader easing in global inflation pressure which will benefit Australia and it highlights that monetary policy still works in slowing inflation and so there is no reason why it shouldn’t work here too.

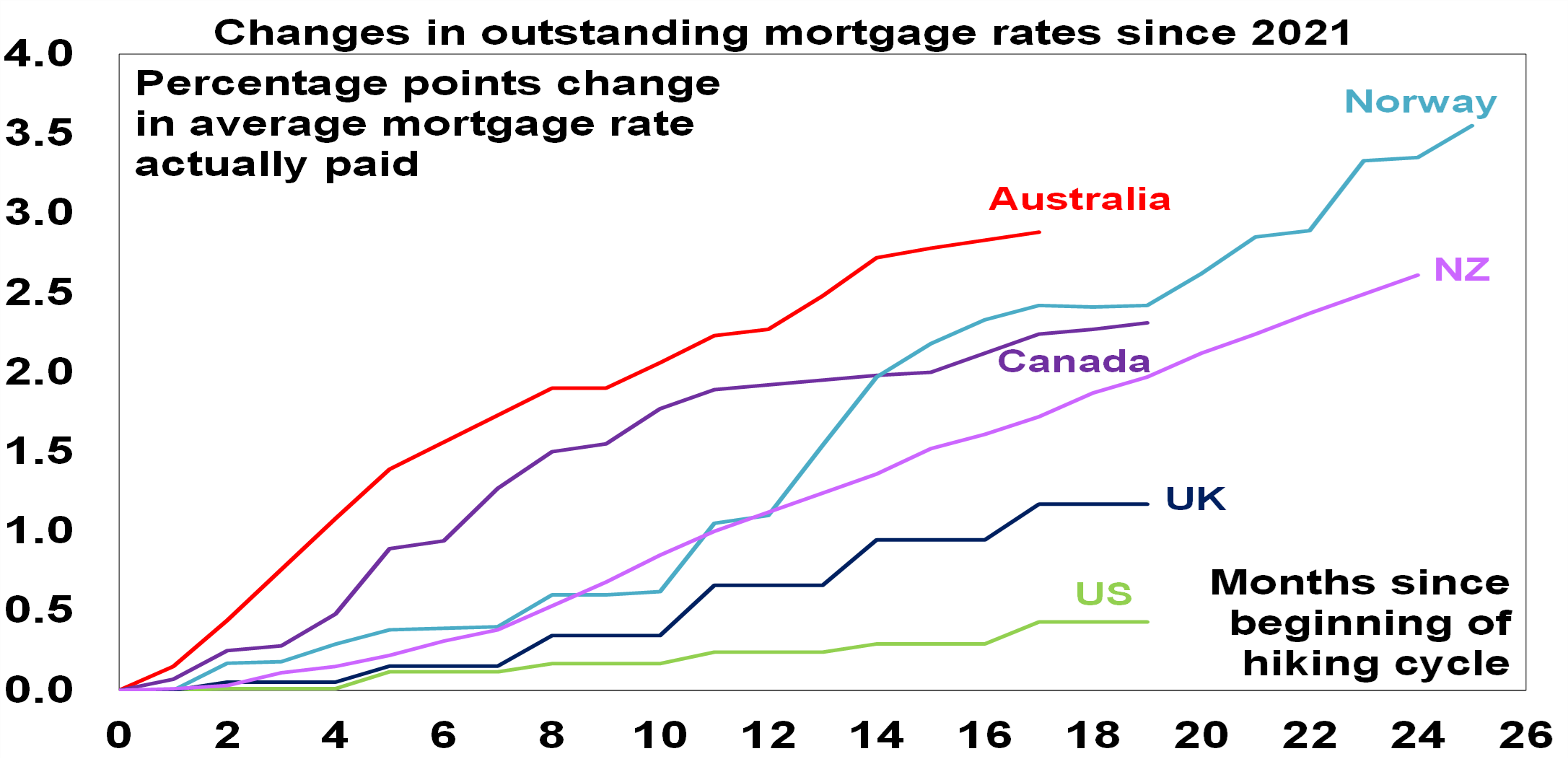

Finally, it should be noted that while the RBA has not raised its key policy rate as much as in other comparable countries (5% in Canada, 5.25% in the UK, 5.37% in the US & 5.5% in NZ), the rise in actual outstanding mortgage rates exceeds that in most other countries (reflecting the higher reliance on short dated borrowing here) implying a much bigger hit to households.

Note this data is mostly only available up to Sept/Oct. Source: Macrobond, RBA, AMP

Concluding comment

The short-term risk for interest rates still remains on the upside given the RBA’s own tightening bias – so we are allowing for a 40% risk of another hike which would most likely come in February if it occurs. Yet continuing to raise interest rates will only add to the already very high risk of recession, particularly given the uncertainty around the long and variable lags with which rate hikes impact the economy meaning that there is a big impact yet to fully show up. As a result, the economy is likely to slow further into next year which along with supply chain improvements is likely to push headline inflation down to three point something earlier than the RBA is allowing. As a result, our base case is that the cash rate has peaked with rate cuts starting in the second half of next year. Key to watch will be the global economy, household spending, inflation and the labour market.

Dr Shane OliverHead of Investment Strategy and Chief Economist, AMP

What you need to know

While every care has been taken in the preparation of this article, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This article is solely for the use of the party to whom it is provided and must not be provided to any other person or entity without the express written consent AMP. This article is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.

The information on this page was current on the date the page was published. For up-to-date information, we refer you to the relevant product disclosure statement, target market determination and product updates available at amp.com.au.

![]()